Written by Tony Sondhi; A. C. Sondhi & Associates, LLC, September 26, 2016

Comments on SEC Staff Announcement on SAB Topic 11.M (SAB 74)

On September 22, 2016, the SEC Staff issued comments on the disclosure requirements of SAB Topic 11.M (SAB 74) related to the expected impact on financial statements of the future adoption of the following recently issued accounting standards:

- ASU 2014-09, Revenue from Contracts with Customers (Topic 606),

- ASU 2016-2, Leases (Topic 842), and

- ASU 2016-13, Financial Instruments – Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments.

SAB Topic 11.M (SAB 74) requires disclosure of the potential material effects of newly issued standards when those are adopted. In addition to the general statement of the lack of sufficient information or the inability to reasonably estimate the expected impact on the financial statements, the Staff asked registrants to consider additional qualitative disclosures to:

- Address the effect of accounting policies the registrant expects to use, if determined,

- Provide a comparison to current accounting policies, and

- Describe the status of the implementation process and significant implementation matters that have not yet been addressed.

The SEC Staff is expected to review Topic 11.M (SAB 74) disclosures for the next annual period and the disclosures are encouraged for upcoming quarterly filings.

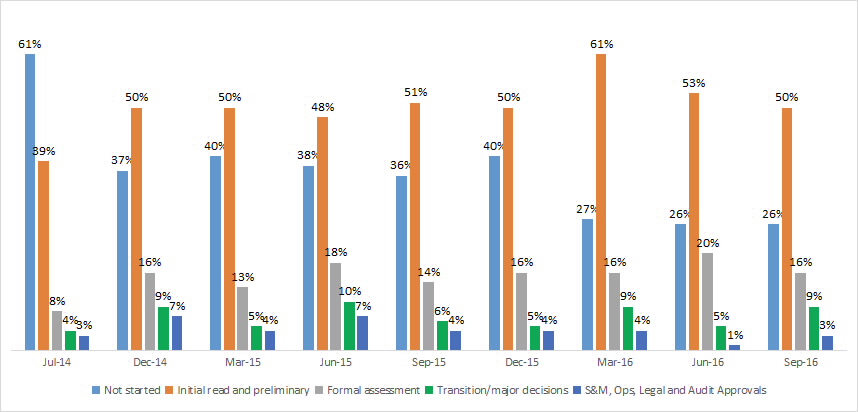

Beginning with our monthly webcast in July 2014, Silicon Valley Accountants (my sponsors) and I have tracked the status of the implementation process as it relates to ASU 2014-09, Revenue from Contracts with Customers (Topic 606).

Here are the results to date:

Assessment (Phase I) – Adoption process & Disclosure – ASU 2014-09 (Topic 606)

*Note: This survey asked respondents to select all that apply. Therefore, the results total to more than 100%

The first stage, not started assessment, applies to entities that have not yet begun formal work on implementation. The entities may have reviewed the standard and attended some webcasts or training sessions. Entities with a basic project plan have reached the next stage, initial read and preliminary assessment. The third stage, formal assessment, includes entities whose senior management has agreed to a more comprehensive plan, the core implementation team, and the tasks for the lead Finance and accounting team as well as those for contracts personnel and other teams have been determined (in some cases, portion of the work may have been completed). The transition/major decisions level of progress in the implementation project refers to final decisions on the transition approach to be used (full or modified retrospective) and completed work on accounting policies to be used, documentation and IT needs are nearly final, and agreement has been reached on the cost capitalization issues. The final stage companies have completed the work and obtained approvals from various stakeholders. These companies may have begun and some may have completed the test phases.

Please note that our audience changes from month to month and some of the variation in results is due to the topic addressed in a webcast; not all webcasts were devoted to ASU 2014-09. Our experience suggests that many companies face a difficult challenge in meeting SAB 74 disclosure requirements early next year when they file their financial statements. It is time to get to work on the implementation projects. It is also important to start thinking about and drafting your SAB 74 disclosures.

Please call me at 727-797-1515 or email me for information about our consulting and advisory services related to the implementation of these standards.

If you’d like to participate in this survey, we’d appreciate your input. Click here for the survey: